As part of the newly published proposed budget are significant cuts to research and the prime target are indirect expenses, what seems to be a slush fund to some and a critical financial asset to others.

“I was struck by one thing at NIH,” Price said, “and that is that about 30 percent of the grant money that goes out is used for indirect expenses, which as you know means that that money goes for something other than the research that’s being done.” [1]

Widely cited in this discussion are figures noting indirect cost payments of 27.9% ($6.6 billion out of $23.5 billion) or Johns Hopkins receiving $156 million in indirect costs associated with $1.05 billion in research and teaching awards (14.8%). The rationale for reduction in ‘overhead payments” is

"These so-called indirect costs, which are paid at rates now negotiated between individual institutions and the government, currently comprise about 30% of NIH’s total grant funding. The variable indirect cost rates would be replaced with a uniform rate of 10% of total research costs for all NIH grants to reduce paperwork and “the risk for fraud and abuse,” states a budget document for the Department of Health and Human Services (HHS). A 10% cap would bring NIH’s indirect costs rate “more in line” with the rate paid by private foundations such as the Bill & Melinda Gates Foundation, the overall budget document notes. NIH will also work to reduce regulatory burdens on grantees." [2]

But before we reduce these indirect costs, what are they really and how do we currently negotiate them? This information comes from Sally Rockey, who was Deputy Director of Extramural Research and Director of the Office of Extramural Research (OER) at the NIH when she recorded her comments.

Indirect costs (IDC) are costs that cannot be directly accounted for as part of the funded research

- IDC includes an administrative component paying a portion of a University’s general administration costs as well as parts of the administration expenses of the particular department involved in the research and a portion of the administrative expenses for the unit within the University responsible for applications and compliance with research grants. It also includes graduate student services. These costs are capped at 26% of the total grant and have been since 1991

- IDC includes facilities costs - building debt and depreciation, equipment depreciation, operations and maintenance e.g. lights, security, heat.

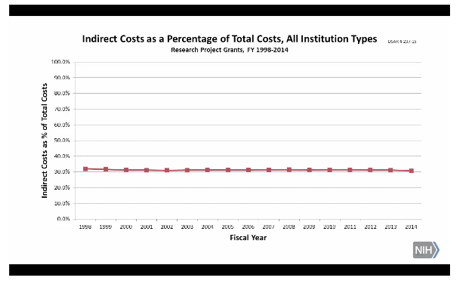

- IDC have been flat or slightly decreased since 1998

- Since 1996 IDC rates are subject to negotiation by either Health and Human Services Division of Cost Allocation (dealing primarily with NIH research grants) or the Department of Naval Research (dealing mainly with Department of Defense research grants).

- Since 2014 all the rules governing the definitions and negotiations for IDC are codified in a Uniform Guidance report, and the only exceptions to those standards are because of regulatory statutes or direct approval of the agency head – neither is a common practice.

The first lesson is that this is an area addressed by the government for easily 25 years. It has been standardized and overseen and searching for abuse is one of the consistent and persistent goals. Can we realistically expect to find and realize hidden significant savings?

To be fair, indirect costs can be a bit fuzzy. For instance, there is some financial incentives to place research in a lovely new building that comes with a lot of debt and large depreciations. Those costs are indirect and not capped. But the ‘real’ problem revolves around the University’s business model; it has three different markets (models) under one roof. There is the business of teaching undergraduates, the teaching of graduates, and research. Each business has different expenses and outcomes and

...when running several business models simultaneously, there is great opportunity for cost shifting from one component to another when the organization wants to discreetly cross subsidize activities. It thus becomes very difficult, if not impossible, for customers to understand exactly what they are paying for. [3]

If the President’s proposal is successful, then you can anticipate that Universities will shift those costs elsewhere, to among other places tuition. The painful truth is that cutting IDC doesn’t reduce our spending; it shifts it. And in this case, the shift will be from the large group of taxpayers to the smaller group of university students (and their parents). This is robbing Peter to pay Paul, and you have to ask yourself whether students with an average of $37,172 in loan debt can afford more? And you have to ask can government and universities find methods other than cost shifting to bring about real savings?

[1] https://www.statnews.com/2017/03/29/tom-price-nih-budget/

[2] http://www.sciencemag.org/news/2017/05/what-s-trump-s-2018-budget-request-science

Chuck Dinerstein, MD, MBA

Director of Medicine

Dr. Charles Dinerstein, M.D., MBA, FACS is Director of Medicine at the American Council on Science and Health. He has over 25 years of experience as a vascular surgeon.