Medicare Advantage’s Value Proposition

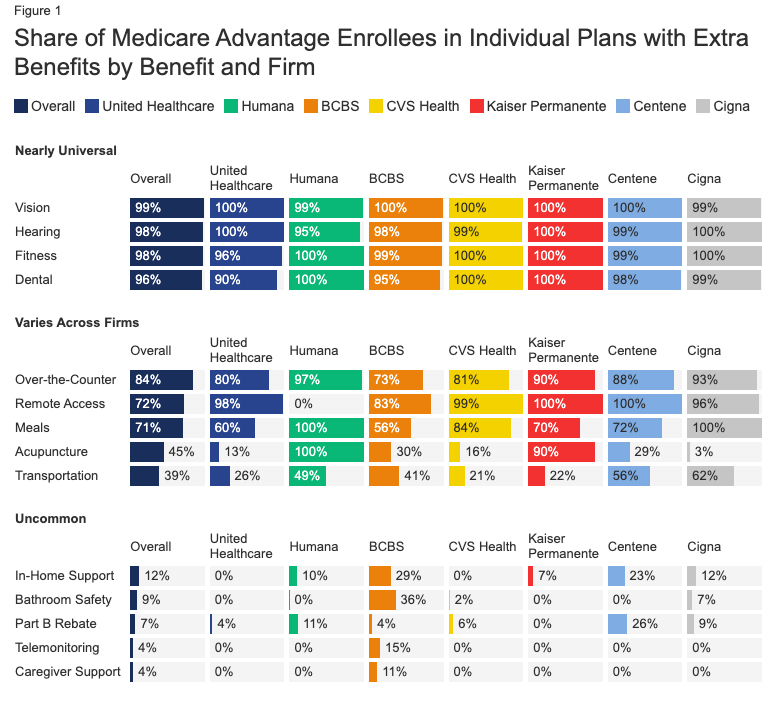

If you believe TV commercials, Medicare Advantage (MA) programs are fantastic. For no additional cost, and in some cases for a reduction in Medicare premiums, beneficiaries get their Medicare benefits and other health perks. Those perks include free vision and hearing care, including eyeglasses and over-the-counter medications and supplies for some.

A decade ago, MA had enrolled roughly 25% of beneficiaries; now, it has enrolled 41% of Medicare beneficiaries, about 26.2 million. And those numbers, according to the Congressional Budget Office, should exceed 50% by 2026. According to CMS, 90% of beneficiaries are enrolled in MA plans with a 4.5-star rating or higher. [1]

Star ratings are given for programs that meet CMS guidelines, such as the number of patients with elevated cholesterol on statins, etc. Over the years, there has been some grade inflation, just as we find in high schools. In 2013, 38% of plans had four stars or more, now 50% have that rating. And as I and others have written, it is easy for the insurers to game the system. In a scenario reminiscent of bankers who folded bad mortgage debt into good mortgage debt, insurers are bundling lower-rated plans into higher ones. Would it surprise you that attaining four or more stars comes with a bonus payment? Those bonuses come to $11.6 billion this year.

Medicare Advantage’s Mathmagic

How do MA programs seem to magically wring costs out of Medicare and provide more benefits? Is there a goose laying a golden egg? Perhaps metaphorically. MA programs receive payments from Medicare to cover all the costs incurred by their beneficiaries over the year. Don’t spend all the money, and it accrues to the insurers; spend more than that, and the debt falls to the insurers – as Nassim Taleb would say, they have “skin in the game.”

Of course, payments are based on the beneficiary's underlying medical needs and risk; the insurers receive greater payments for those that are more ill – at least on paper. The severity of illness is based on documentation, and the insurers try to “up code” the severity of illness in all ways possible.

“Just imagine that a bond is a slice of cake, and you didn’t bake the cake, but every time you hand somebody a slice of the cake a tiny little bit comes off, like a little crumb, and you can keep that. […] If you pass around enough slices of cake, then pretty soon you have enough crumbs to make a giganticake”…Golden cake. And Pierce and Pierce collects millions of marvelous- she shrugged- “golden crumbs.” Bonfire of the Vanities

The other means of cost control are through payments to hospitals and “providers.” Under Medicare, hospital payments are based upon the admitting diagnosis, and provider payments are based upon services provided. For those institutions and individuals who “participate” in the Medicare Program, that means they will receive a check for 80% of the allowable charges directly from Medicare; the remaining 20% comes from the individual or their insurance. MA programs step on those percentages and take a “few golden crumbs.” They do so by their increasing market size, offering hospitals and providers a different value proposition – we will give you our patients, but you will receive discounted Medicare fees. [2]

The other means of cost control are through payments to hospitals and “providers.” Under Medicare, hospital payments are based upon the admitting diagnosis, and provider payments are based upon services provided. For those institutions and individuals who “participate” in the Medicare Program, that means they will receive a check for 80% of the allowable charges directly from Medicare; the remaining 20% comes from the individual or their insurance. MA programs step on those percentages and take a “few golden crumbs.” They do so by their increasing market size, offering hospitals and providers a different value proposition – we will give you our patients, but you will receive discounted Medicare fees. [2]

Of course, many providers and some health systems do not take the discounted rates, so the facilities and physicians available to MA beneficiaries are more limited – the term used is “narrow networks.” As a result, an individual’s physician may participate in Medicare, but not in Medicare Advantage, and when those physicians are seen, additional fees are charged to the patient.

The profitability of MA programs accrue because of subtle upcoding to increase the government’s underlying payments, gaming the system to qualify for government “bonus payments” based upon ill-conceived quality standards, and reducing the payments to hospitals and providers. In the end, the “free lunch” that Medicare Advantage provides is paid for by taxpayers, health facilities, and providers. The “cost” borne by MA beneficiaries is in their narrowed selection of caregivers. As the Government Accountability Office has indicated, 5% of beneficiaries in the final year of their life return to Medicare because the services they need in those final days are difficult to get.

Those of us over 65 find it hard not to consider that free lunch, especially those engaging ads that tell us that we will be not only getting free services but might also get a reduction in our costs – can we be blamed for wanting more for less? But from a policy point of view, do we want this to be the result? Medicare becoming the “public option,” and the Medicare Advantage programs represent revenue streams to large health insurers.

[1] There are a total of five starts

[2] This is beyond the scope of today’s article, but it has to do with market share and the fees being paid by other health plans. In many cases, it is exceedingly difficult to collect that additional 20% from patients, so the effective Medicare reimbursement may well be 85-90% of the agreed-upon payment.

Chuck Dinerstein, MD, MBA

Director of Medicine

Dr. Charles Dinerstein, M.D., MBA, FACS is Director of Medicine at the American Council on Science and Health. He has over 25 years of experience as a vascular surgeon.