In complex systems, intermediaries can “grease the wheels” by lowering transaction costs, streamlining logistics, and bridging information gaps. In healthcare, much of the recent attention has focused on pharmacy benefit managers (PBMs), the current villains in our overly expensive system.

Medicare Advantage has frequently appeared in the news cycle amid concerns about risk-score upcoding, its growing enrollment and costs relative to traditional Medicare, and proposals by the Trump Administration to make it the default option for new Medicare beneficiaries. That attention should extend to another healthcare intermediary: the Medicare Advantage (MA) insurance broker.

To understand why brokers matter, start with the problem facing any new Medicare beneficiary: too many plans, too much fine print, and too little time to compare them all.

A Market Built for Middlemen

With over 40 plans, MA insurance brokers help bridge the information gap between buyers and sellers and, in economic terms, lower search costs for both new beneficiaries and MA plans, making the market “more efficient.” Theoretically, by handling the logistics of discovery and onboarding for new beneficiaries, they allow health plans to focus on their core role in financing health coverage.

MA insurance brokers may be self-employed, work for independent agencies, or be employed by specific health plans. It is tempting to assume that employed brokers are more likely to steer clients toward their own company’s plans, while independent brokers are free from such conflicts. But neither group is a fiduciary—that is, neither is legally required to act solely in the best interest of the Medicare beneficiary seeking coverage.

A study in JAMA Internal Medicine, based on a Freedom of Information Act request, sheds badly needed light, allowing us to “follow the money” by providing the first reasonable estimate of how many beneficiaries use MA insurance brokers and how much money is exchanged. The study’s importance lies in a simple fact: beneficiaries usually do not see the broker bill, but the money still comes from somewhere.

Medicare beneficiaries do not pay brokers directly. Broker commissions are capped by federal regulation at $611 for new subscribers and $306 for annual renewals in the same plan. But those commissions are still paid—by Medicare Advantage plans. Plans cover such administrative and sales costs from the share of premium revenue they retain for overhead and profit. Because Medicare Advantage is substantially funded by the federal government, taxpayers ultimately help finance those commissions. Beneficiaries may not see the bill, but the money still comes from the Medicare system.

The financial term for this is an intermediated settlement, in which payments do not go directly from buyer to seller but pass through clearinghouses, brokers, or escrow agents. Once those indirect payments are made visible, the next question is not whether brokers are paid, but what they are paid for.

Following the Money

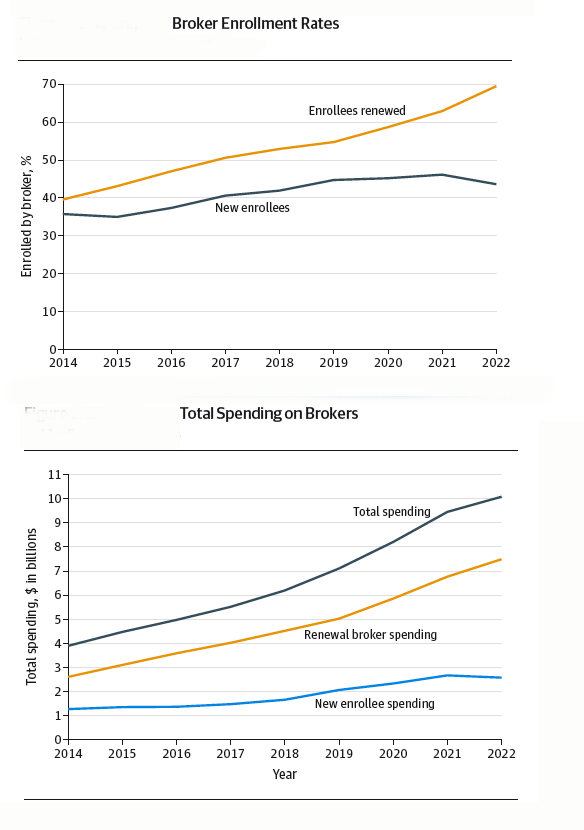

- From 2014 to 2022, there were 22 million new enrollments and 112 million renewal enrollments, with the proportion of broker-mediated referrals rising from 35% to 43%.

- The proportion of enrollees who remained in their plan, generating a renewal fee, rose from 50% to 69%.

- Broker commissions increased from an estimated $3.9 billion to $10.1 billion, of which 73% were renewal commissions.

[1]

[1]

“The Rent is Too Damn High”

Brokers may face conflicts of interest when enrolling Medicare beneficiaries, especially if one plan pays more or is easier to sell than another. Still, initial enrollment can involve real work: explaining benefits, comparing premiums, checking networks, and helping beneficiaries complete paperwork. The sharper question concerns what happens after that first enrollment.

There is a fairly consistent “churn and burn” among MA recipients, with up to 50% switching plans within 5 years of joining and 10% returning to traditional Medicare. [2] Some of that movement may reflect changing health needs, benefit changes, network disruptions, or dissatisfaction. But for those who remain in the same plan, the key question is straightforward: what service does the broker provide when a renewal commission is paid?

Jimmy McMillan, a perennial candidate for NY City Mayor, ran as the candidate of the Rent is Too Damn High Party. While he spoke long before NYC’s current mayor and focused on housing rent, economic rent can be defined as unearned revenue or payment made to a service provider that exceeds the actual costs, competitive prices, or opportunity costs required to bring or keep that resource in service.

For MA brokers, renewal fees can function as economic rent when they are paid automatically rather than tied to documented annual service. The commission is generated when a beneficiary remains in an existing plan, even if the broker did little or nothing to help that person reassess coverage.

These recurring payouts may require minimal additional labor from the broker, especially when no active plan review occurs. That institutional setup creates a lucrative positional advantage: renewal commissions can compound into a passive revenue stream that, according to the JAMA Internal Medicine estimate, accounts for 73% of broker fees.

That does not mean brokers see the issue this way.

Brokers Push Back

If the MA brokers are the landlords in my “too much rent” metaphor, the tenants, the federal government and insurers, hold more divergent views. The Biden Administration sought to limit Medicare Advantage broker compensation, but courts found that effort exceeded the agency’s regulatory authority. UnitedHealthcare and other insurers have eliminated some commissions for independent brokers, though how they compensate employed brokers remains less transparent. Brokers, meanwhile, argue that cutting commissions would harm the very beneficiaries the policy is supposed to protect. The National Association of Insurance and Financial Advisors, or NAIFA, put it this way

“Licensed Medicare advisors are vital. They serve as year-round advocates who help clients compare plan options, navigate changing benefits, address denials, and adjust coverage to meet evolving needs. Stripping away their compensation … jeopardizes seniors’ ability to make informed decisions in a system that is already complex and confusing.”

- NAIFA CEO Kevin Mayeux

That defense is strongest when brokers provide year-round advice; it is weaker when commissions arrive simply because a beneficiary stays put.

Medicare Advantage brokers may help seniors navigate a confusing marketplace. But how much help are we actually buying? When 73% of a multi-billion-dollar payout comes from automatic renewals, broker compensation starts to look less like payment for service and more like a toll. Are we funding advocacy, or annuities? Taxpayer-subsidized healthcare dollars should be buying clinical care and real guidance—not quietly feeding administrative machinery that pays itself year after year.

[1] The figure is an estimate because payments to employed brokers are unknown, and the analysis used the capped commission amount.

[2] In these circumstances, a broker may receive a much higher enrollment commission from the new MA plan than the renewal commission from the existing plan.

Source: Trends in Broker Enrollment and Spending in Medicare Advantage JAMA Internal Medicine DOI: 10.1001/jamainternmed.2026.0864

Chuck Dinerstein, MD, MBA

Director of Medicine

Dr. Charles Dinerstein, M.D., MBA, FACS is Director of Medicine at the American Council on Science and Health. He has over 25 years of experience as a vascular surgeon.